By ALEX KENNEDY, Associated Press – 1 hr 48 mins ago

SINGAPORE – Oil prices rose to near $102 a barrel Tuesday in Asia as a weakening U.S. dollar made crude cheaper for investors with other currencies.

Benchmark oil for July delivery was up $1.27 to $101.86 a barrel at late afternoon Singapore time in electronic trading on the New York Mercantile Exchange.

The benchmark contract last settled Friday up 36 cents at $100.59. Markets in the U.S. were closed Monday for the Memorial Day holiday.

In London, Brent crude for July delivery was up $1.04 to $115.72 a barrel on the ICE Futures exchange.

Crude has risen from $96 last week amid a depreciating U.S. currency. The euro rose to $1.4406 on Tuesday from $1.4287 late Monday.

"Bottom line, as goes the dollar, so goes oil, in the opposite direction," energy consultant The Schork Group said in a report.

Traders are also eyeing the U.S. economy, where recent manufacturing and consumer spending indicators have been less than robust.

However, sluggish economic indicators are a mixed signal for oil traders. A weaker economy would suggest less demand for crude, but it also tends to reduce confidence in the dollar, and a falling U.S. currency usually boosts oil prices.

"The strength and sustainability of the U.S. recovery is in question," The Schork Group said. "But the Catch-22 is poor economic headlines are actually supporting higher oil prices vis-a-vis the U.S. dollar."

Oil has dropped from a 30-month high near $115 a barrel on May 2.

In other Nymex trading in June contracts, heating oil gained 2.3 cents to $3.01 a gallon and gasoline added 2.7 cents at $3.12 a gallon. Natural gas futures rose 7.7 cents to $4.60 per 1,000 cubic feet.

Tuesday, May 31, 2011

Monday, May 30, 2011

Have Gold Prices Stopped Falling? - 27 May 2011

Record highs in Euro gold prices suggest the market has found a floor...

WE'VE SEEN Gold Prices fall from $1,578 to $1,492 in recent weeks – a 5.45% drop. Gold Prices in the Euro it fell from €1,065 to €1,042 – a fall of 2.16%. The fall of gold in the Euro painted a more accurate reflection of supply and demand, because the Dollar rose against the Euro, as gold was falling, reckons Julian Phillips at GoldForecaster.

This was simply a correction, provided the Gold Price has stopped falling now. A fall of 10% is a proper correction and a mid-trend correction fall should be around 20 to 30%.

The fall appears to have been caused by a big investor and his following virtually dumping around 37 tonnes in a two week period into a market that is used to seeing around 6 tonnes a day from the producers.

Pity he didn't have a better dealer. This seller appears to have completed his sales (if it was George Soros, then he has completed them, for he only held 30 tonnes apart from gold shares).

The fall from just about $50 to $32 rattled the entire market. After all, a fall of 36% is a major trend correction were it broad based from many investors over a period.

But this drop was again due to awful dealing with 1,000 tonnes from the Silver Trust's holdings coming onto the market over two weeks, with the bulk dumped into the market in the second week together with another 7 tonnes from similar thinkers.

With the Silver Price back above $37 the drop is now down to a fall of 26% from the peak of $50. Again the selling has largely stopped with two-way traffic now in play.

The gold market is a global, well centralized market based in London, where heavy sellers and buyers are brought together quickly and a well-priced deal made that cuts out the bulk of the volatility we see in the silver market.

The London Fix is where potential buyers and sellers of physical gold sit on the end of their telephones twice a day and see what's on offer and what the bids are for it. Even the appearance of a large amount such as we saw from the States is swallowed up quickly and in an orderly fashion.

The value of an ounce of gold at 41 times the price of an ounce of silver increases the liquidity for the big players in the market, making it easier to move large amounts quickly.

Silver has nowhere near that level of liquidity or depth of investors. The type of investor is wide from institutions to industry from the small investor to the large one and a fully global market at that.

However, the day-to-day dealings, while well-organized, are not sufficiently large in two-way traffic to accommodate the sudden appearance of 1,000 tonnes in two weeks. This is why the market is so volatile and swings so widely, compared to the gold market.

The silver market will, over time, see a lessening of volatility once prices are higher and silver more accepted as a precious metal more closely linked to gold. We would then expect to see Silver Prices move far closer to those of gold.

Bearing in mind that the fundamentals for silver's traditional uses and industrial applications are either for investment, jewelry or much needed applications in industry, the fundamentals for silver are just as they were while the Silver Price was rising and are unlikely to change. These users will be delighted with any pullback, but tend to be price-insensitive.

That means they need silver no matter what the price. As to the investment demand for silver, this is at its largest from the emerging world and is likewise relatively price-insensitive. People from this part of the world are buying in line with their increasing income and ability to buy. The price rises have simply confirmed the wisdom of such a policy.

The same applies to the gold market, but with the added feature that central banks are buyers as well. These too are price-insensitive buyers, simply taking up gold as it appears on the market, without chasing prices.

The prices of both gold and silver have risen from their recent bottoms and have begun to rise. This is a classic 'floor' finding exercise.

Silver has been the slower mover and has waited for gold to lead the way. In the Dollar the Silver Price is recovering and is now moving through the $37 level. In the Dollar the Gold Price still has another $50 to rise to its peak levels too. This is another 3% more. Silver at $37 still has to rise another 26% to reach its peak.

But what is hiding their moves has been the rally in the Dollar itself. In the Euro silver fell from €33.56 to €22.53 a fall of 33%. It now stands at €26.3 a fall of 21.6%. This shows it is recovering faster in percentage terms, once we extract the Dollar gyrations.

It is clear then that support is now effective and holding up both the prices of gold and silver in the market. Especially if we look at the Euro Gold Price – which set a new record high this week.

WE'VE SEEN Gold Prices fall from $1,578 to $1,492 in recent weeks – a 5.45% drop. Gold Prices in the Euro it fell from €1,065 to €1,042 – a fall of 2.16%. The fall of gold in the Euro painted a more accurate reflection of supply and demand, because the Dollar rose against the Euro, as gold was falling, reckons Julian Phillips at GoldForecaster.

This was simply a correction, provided the Gold Price has stopped falling now. A fall of 10% is a proper correction and a mid-trend correction fall should be around 20 to 30%.

The fall appears to have been caused by a big investor and his following virtually dumping around 37 tonnes in a two week period into a market that is used to seeing around 6 tonnes a day from the producers.

Pity he didn't have a better dealer. This seller appears to have completed his sales (if it was George Soros, then he has completed them, for he only held 30 tonnes apart from gold shares).

The fall from just about $50 to $32 rattled the entire market. After all, a fall of 36% is a major trend correction were it broad based from many investors over a period.

But this drop was again due to awful dealing with 1,000 tonnes from the Silver Trust's holdings coming onto the market over two weeks, with the bulk dumped into the market in the second week together with another 7 tonnes from similar thinkers.

With the Silver Price back above $37 the drop is now down to a fall of 26% from the peak of $50. Again the selling has largely stopped with two-way traffic now in play.

The gold market is a global, well centralized market based in London, where heavy sellers and buyers are brought together quickly and a well-priced deal made that cuts out the bulk of the volatility we see in the silver market.

The London Fix is where potential buyers and sellers of physical gold sit on the end of their telephones twice a day and see what's on offer and what the bids are for it. Even the appearance of a large amount such as we saw from the States is swallowed up quickly and in an orderly fashion.

The value of an ounce of gold at 41 times the price of an ounce of silver increases the liquidity for the big players in the market, making it easier to move large amounts quickly.

Silver has nowhere near that level of liquidity or depth of investors. The type of investor is wide from institutions to industry from the small investor to the large one and a fully global market at that.

However, the day-to-day dealings, while well-organized, are not sufficiently large in two-way traffic to accommodate the sudden appearance of 1,000 tonnes in two weeks. This is why the market is so volatile and swings so widely, compared to the gold market.

The silver market will, over time, see a lessening of volatility once prices are higher and silver more accepted as a precious metal more closely linked to gold. We would then expect to see Silver Prices move far closer to those of gold.

Bearing in mind that the fundamentals for silver's traditional uses and industrial applications are either for investment, jewelry or much needed applications in industry, the fundamentals for silver are just as they were while the Silver Price was rising and are unlikely to change. These users will be delighted with any pullback, but tend to be price-insensitive.

That means they need silver no matter what the price. As to the investment demand for silver, this is at its largest from the emerging world and is likewise relatively price-insensitive. People from this part of the world are buying in line with their increasing income and ability to buy. The price rises have simply confirmed the wisdom of such a policy.

The same applies to the gold market, but with the added feature that central banks are buyers as well. These too are price-insensitive buyers, simply taking up gold as it appears on the market, without chasing prices.

The prices of both gold and silver have risen from their recent bottoms and have begun to rise. This is a classic 'floor' finding exercise.

Silver has been the slower mover and has waited for gold to lead the way. In the Dollar the Silver Price is recovering and is now moving through the $37 level. In the Dollar the Gold Price still has another $50 to rise to its peak levels too. This is another 3% more. Silver at $37 still has to rise another 26% to reach its peak.

But what is hiding their moves has been the rally in the Dollar itself. In the Euro silver fell from €33.56 to €22.53 a fall of 33%. It now stands at €26.3 a fall of 21.6%. This shows it is recovering faster in percentage terms, once we extract the Dollar gyrations.

It is clear then that support is now effective and holding up both the prices of gold and silver in the market. Especially if we look at the Euro Gold Price – which set a new record high this week.

Thursday, May 26, 2011

Dollar Rebound Hinted as Stock Positioning Points to Collapse in Risk Appetite

By Ilya Spivak, Currency Strategist

25 February 2011 03:48 GMT

US DOLLAR INDEX – The greenback is testing trend-defining support at a rising trend line set from the record low in March 2008, with a break lower amounting to a material bearish shift in long-term positioning. Likewise, the boundary is a logical place for a reversal higher and the currency’s behavior here over the coming days and weeks will be critical in determining where the benchmark unit (and the major currencies in general) are heading.

MSCI WORLD STOCK INDEX – Prices are testing a critical support level at the confluence of two significant trend lines – a longer-term one set from August and a minor one dating back to December – as well as 23.6% Fibonacci retracement of the rally from the late-November swing bottom. Negative RSI divergence hints the path of least resistance favors the downside, suggesting a major collapse in market-wide risk appetite may be just around the corner.

CRUDE OIL – Prices spiked higher but overall positioning remains little changed, with crude trapped between the 161.8% Fibonacci extension of the downswing from late January 2010 ($98.40) and a rising trend line connecting major highs since June (now at $95.53). Renewed upward momentum targets the 200% Fib at $101.83 while a break back below the trend line exposes $92.84.

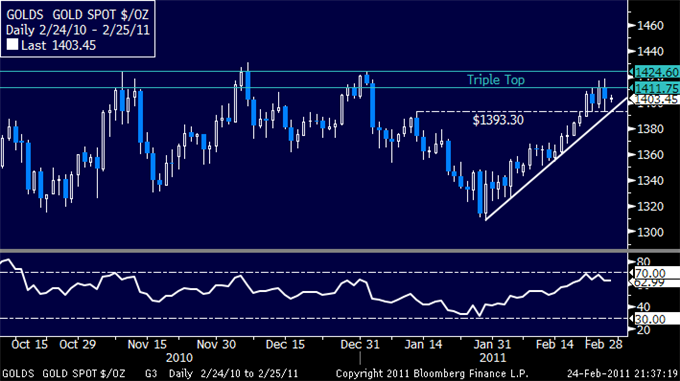

GOLD –Prices continue to consolidate below triple top resistance in the $1411.75-1424.60 region. Negative RSI divergence hints at the likelihood of a downside scenario. Initial support lining up at $1393.30 (the Jan 13 high) and is reinforced by a rising trend line set from the January low. Penetration below this barrier initially exposes $1376.20.

For real time news and analysis, please visit http://www.dailyfx.com/real_time_news

To receive future articles by email, please contact Ilya at ispivak@dailyfx.com

Tuesday, May 24, 2011

THE RINGGIT AND THE DOLLAR

THE RINGGIT AND THE DOLLAR

by Dr. Mahathir bin Mohamad on Thursday, 12 May 2011 at 06:56

1. The dollar i.e. the US dollar has been depreciating against the Ringgit. It is now hovering just below RM3.00 to 1 USD. Obviously this currency crisis is not over yet. Obviously the US is still in trouble. Europe is also in trouble and so is the rest of the world. This is the longest financial crisis in history. It is now in the fourth year.

2. This crisis started in the US in 2008 with the banks going bankrupt because the sub-prime loans defaulted and Lehman Brothers went bankrupt. Since then the US Government has been printing money by the trillions to bail out banks, insurance and automobile companies.

3. Currently Greece is still unable to repay loans caused by the switch to the Euro.

4. Malaysia appears to have escaped much of the crisis. Our currency is in fact getting stronger and our economy is growing at a good rate.

5. Why has a serious currency crisis affected the developed countries and not as much the developing countries? The answer is that we have not been trying to get rich quick through playing the money market.

6. I am not a financier of course and my knowledge about finance can be written on the back of a postage stamp. So no one should take what I say about finance seriously.

7. Still, I would like to hazard a theory.

8. The US was, after the Second World War, the richest nation. They have companies like General Motors, General Electric, Caterpillar Tractors, McDonnell Douglas & Boeing, great manufacturers of household appliances, radios and television, machine tools, precision instruments and of course a massive weapons industry.

9. They were so confident of the superiority of their industries that they did not mind teaching the Japanese the importance of quality and expertise in manufacturing.

10. To cut a long story short, the Japanese mastered manufacturing so well that their high quality but competitive products displaced those of the Americans and much of the Europeans in the world market.

11. After Japan came Taiwan, South Korea and then China. The products of these countries even displaced American and European products in their own countries. The last straw is the invasion of East-Asian cars into the American and European markets.

12. Instead of trying to compete, the Americans in particular, and the Europeans opted to surrender the markets to the Asian newcomers. But American and European economies continued to grow and they remain as prosperous as ever.

13. To remain ahead in wealth the Americans and Europeans invented a new market - the money market. They invented ways of making money from money. These they call products although they cannot be eaten or used.

14. The banking system they created was for the purpose of lending money to finance business enterprises. To do this the banks were allowed to lend more money than they have as capital, assets and deposits. In effect this means the banks could create money. In fact in the past banks issued banknotes to pay for goods and services. Later the banknotes were replaced by cheques. Everything can be paid with cheques. No cash is needed any more.

15. It was fine as long as the Government oversees the money created by the banks and limits it to ten times the banks assets. Then the American Government decided that it should not supervise the banks. The market would regulate itself.

16. Freed of Government oversight the banks began to lend far more than ten times their assets. They lent even to people with no income and no capacity to repay the loans, especially for houses.

17. The loans were then either mortgaged or insured. The belief was that they were safe. In any case if the borrower defaulted the property would be worth more than the loans as property prices seem to appreciate all the time.

18. Other ways of making money were invented. Hedge funds, carry trade, currency trade, mergers and acquisitions, investment in 'emerging markets' (formerly known as developing countries), junk bonds, securitised mortgage, commercial paper, short selling, index funds, sub-prime loans, private equity funds, repo market, structured investment vehicles, etc etc

19. Any of these things can give huge profits. For the astute players any of these things can make them millionaires or billionaires overnight, practically overnight.

20. The money market products yield nothing substantial. They create no jobs, no tangible products, no trade in goods or services, no spin-offs in terms of business, no transportation of goods by land, sea or air.

21. Yet the size of the transactions in monetary terms is mind-boggling. The trade in currencies is said to amount to four (4) trillion US dollars a day. It is the size of the total German productivity for a year. Yet no jobs are created, no goods or services are produced, no movement of anything is seen.

22. Of course the people involved in the trade make billions of dollars. Operating out of tax free havens, they report to no one and pay no tax.

23. The money market players and the billions they make contribute to the high GDP and the Per Capita incomes of America and Europe.

24. Then came the collapse. The bubble bursts. And there was nothing spilling from the burst bubbles.

25. The money market players know nothing about other business, about the production of goods and service, about real trade in these things. Actually all of them have become poor.

26. And so they resort to printing money, to remain rich. But the money they print is as valuable as toilet paper.

by Dr. Mahathir bin Mohamad on Thursday, 12 May 2011 at 06:56

1. The dollar i.e. the US dollar has been depreciating against the Ringgit. It is now hovering just below RM3.00 to 1 USD. Obviously this currency crisis is not over yet. Obviously the US is still in trouble. Europe is also in trouble and so is the rest of the world. This is the longest financial crisis in history. It is now in the fourth year.

2. This crisis started in the US in 2008 with the banks going bankrupt because the sub-prime loans defaulted and Lehman Brothers went bankrupt. Since then the US Government has been printing money by the trillions to bail out banks, insurance and automobile companies.

3. Currently Greece is still unable to repay loans caused by the switch to the Euro.

4. Malaysia appears to have escaped much of the crisis. Our currency is in fact getting stronger and our economy is growing at a good rate.

5. Why has a serious currency crisis affected the developed countries and not as much the developing countries? The answer is that we have not been trying to get rich quick through playing the money market.

6. I am not a financier of course and my knowledge about finance can be written on the back of a postage stamp. So no one should take what I say about finance seriously.

7. Still, I would like to hazard a theory.

8. The US was, after the Second World War, the richest nation. They have companies like General Motors, General Electric, Caterpillar Tractors, McDonnell Douglas & Boeing, great manufacturers of household appliances, radios and television, machine tools, precision instruments and of course a massive weapons industry.

9. They were so confident of the superiority of their industries that they did not mind teaching the Japanese the importance of quality and expertise in manufacturing.

10. To cut a long story short, the Japanese mastered manufacturing so well that their high quality but competitive products displaced those of the Americans and much of the Europeans in the world market.

11. After Japan came Taiwan, South Korea and then China. The products of these countries even displaced American and European products in their own countries. The last straw is the invasion of East-Asian cars into the American and European markets.

12. Instead of trying to compete, the Americans in particular, and the Europeans opted to surrender the markets to the Asian newcomers. But American and European economies continued to grow and they remain as prosperous as ever.

13. To remain ahead in wealth the Americans and Europeans invented a new market - the money market. They invented ways of making money from money. These they call products although they cannot be eaten or used.

14. The banking system they created was for the purpose of lending money to finance business enterprises. To do this the banks were allowed to lend more money than they have as capital, assets and deposits. In effect this means the banks could create money. In fact in the past banks issued banknotes to pay for goods and services. Later the banknotes were replaced by cheques. Everything can be paid with cheques. No cash is needed any more.

15. It was fine as long as the Government oversees the money created by the banks and limits it to ten times the banks assets. Then the American Government decided that it should not supervise the banks. The market would regulate itself.

16. Freed of Government oversight the banks began to lend far more than ten times their assets. They lent even to people with no income and no capacity to repay the loans, especially for houses.

17. The loans were then either mortgaged or insured. The belief was that they were safe. In any case if the borrower defaulted the property would be worth more than the loans as property prices seem to appreciate all the time.

18. Other ways of making money were invented. Hedge funds, carry trade, currency trade, mergers and acquisitions, investment in 'emerging markets' (formerly known as developing countries), junk bonds, securitised mortgage, commercial paper, short selling, index funds, sub-prime loans, private equity funds, repo market, structured investment vehicles, etc etc

19. Any of these things can give huge profits. For the astute players any of these things can make them millionaires or billionaires overnight, practically overnight.

20. The money market products yield nothing substantial. They create no jobs, no tangible products, no trade in goods or services, no spin-offs in terms of business, no transportation of goods by land, sea or air.

21. Yet the size of the transactions in monetary terms is mind-boggling. The trade in currencies is said to amount to four (4) trillion US dollars a day. It is the size of the total German productivity for a year. Yet no jobs are created, no goods or services are produced, no movement of anything is seen.

22. Of course the people involved in the trade make billions of dollars. Operating out of tax free havens, they report to no one and pay no tax.

23. The money market players and the billions they make contribute to the high GDP and the Per Capita incomes of America and Europe.

24. Then came the collapse. The bubble bursts. And there was nothing spilling from the burst bubbles.

25. The money market players know nothing about other business, about the production of goods and service, about real trade in these things. Actually all of them have become poor.

26. And so they resort to printing money, to remain rich. But the money they print is as valuable as toilet paper.

Monday, May 23, 2011

dave stacy

Dave, a staunch Christian from West Virginia, lived in a Muslim community in Dearborn, Michigan, for 30 days.

Before going to live with Shamael and Sadia, Dave had scant interaction with any Muslims. "I picture a woman with a sheet or hat and her face covered," he said. "I think of men with AK-47s." But Dave knew stepping out of his comfort zone was an amazing opportunity. "It's going to put me, probably, in one of the most vulnerable positions I have to be in," Dave explained, "and I expect to really grow from it."

But the cultural discomfort cut both ways: Shamael was uncomfortable with the prospect of Dave's being alone with Sadia. As Shamael explains, "It's just more of a religious custom that one doesn't stay in a room alone with another person from the other sex."

Dave did stay for the full 30 days and began to embrace Muslim culture. He wore traditional Muslim clothing, studied the Koran daily, spoke Arabic, grew a beard and ate Middle Eastern food.

At the end of his 30-day dare, Dave had a much different perspective about Islam. "Before, I never really knew anything about Islam and I really never had any thoughts of it. I got married, actually, on September 15, four days after 9/11. I just was so angry right after that event!" Dave admits. "It's a very shallow view: 'Muslims hate us. We hate them. Why don't we just nuke them?' There's never really any thought past that. Unfortunately, people that are so ignorant of the other faiths are often the ones that are most vocal about it."

Now, after essentially becoming a Muslim for 30 days, Dave has a new understanding of prejudice. "I've got a new appreciation for what it's like to be discriminated against," says Dave. "When I was in Michigan, it was strange because the white Americans there looked at me very differently [when I was dressed like a Muslim,] often with very mean looks on their faces. [Meanwhile,] the Muslim population was very, very distrustful of me. They thought I was part of some conspiracy to make them look bad."

Of course, this was an interesting experience for Dave's hosts as well.

Shamael says that he found it difficult when he informed Dave of the rules preventing unmarried men and women from being alone together. "As a host, we should be welcoming and we should be inviting— it doesn't matter who it is," explains Shamael. "But with the religious and cultural upbringing we have, we felt it was the appropriate thing to tell him. 'Okay, the man has to go or the woman has to go.' Men and women just don't stay together in one room alone."

In another eye-opening experience, Shamael recounts a conversation he had with Dave. "I asked him a question. I said, 'Name five Muslims that you know,'" Shamael says. "He told me, 'Osama bin Laden, Saddam Hussein...' And I'm, like, 'Oh, my God: We're all terrorists.' And I said, 'What about Muhammad Ali? What about Hakeem Olajiwan? What about these more prominent Muslim figures in America?' And I realized, at that point, Muslims need to do a better job about explaining their faith, about being better American citizens, about taking the lead in addressing different social issues and whatnot."

Saturday, May 21, 2011

Zimbabwe To Trade Diamonds For Gold As It Prepares To Launch Gold-Backed Currency

Submitted by Tyler Durden on 05/20/2011 11:35 -0400

Hyperinflation

International Monetary Fund

Reserve Currency

World Bank

A week ago we presented the idea floated by once hyperinflationary Zimbabwe, oddly jeered by most, that the country is seeking to move to a gold-backed currency, adding, somewhat surrealistically, that the "days of the US dollar as the world's reserve currency are numbered." And if anyone should know a hyperinflationary basket case, it's Zimbabwe. Well, today this bizarre story just went fuller retard, after the country announced that it may exchange diamonds for gold "so that it can have a gold-backed currency, according to a recent proposal from the governor of Zimbabwe’s central bank." Indeed we speculated previously why: "Zimbabwe, a country rich in natural resources, took so long to figure out that it was nothing but a puppet in the hands of western monetary interests." Well, others are now getting this idea - Commodity Online reports that "The country is a resource hub: It sits on gold reserves worth trillions. It has the world’s second largest reserves of platinum, has got alluvial diamonds that can fetch the nation $2 billion annually and even boasts of chrome and coal deposits." And since Zimbabwe is now fully on board this whole "pioneering" thing perhaps it should just go ahead and create the first diamond-platinum backed currency. Just don't give China and Russia ideas about floating a new reserve currency that actually has real commodity backing. What's that, you say? They are launching one soon? Oh well.

From Commodity Online:

The Zimbabwean dollar is no longer in active use after it was officially suspended by the government due to hyperinflation. The United States dollar, South African rand, Botswanan pula, Pound sterling, and Euro are now used instead. The US dollar has been adopted as the official currency for all government transactions with the new power-sharing regime, says Wikipedia.

But the central bank of Zimbabwe—Reserve Bank of Zimbabwe (RBZ)—believes that the US dollar is no longer stable.

According to Dr Gideon Gono, RBZ Chief, the inflationary effects of United States’ deficit financing of its budget may impact foreign countries and would lead to a resistance of the green back as a base currency; cited newzimbabwe.com.

Writing in a blog in New Zimbabwe, Gilbert Muponda, an entrepreneur based out of Zimbabwe has welcomed the proposal of a gold-backed Zimbabwean currency. He has applauded the proposal of the central bank governor to sell diamonds for gold.

On the other hand, for the country to move to some semblance of a gold standard, it may wish to consider shifting form a despotic dictatorship controlled by Robert Mugabe to something a little less "centrally planned."

The government’s protectionist measures have kept the mining companies at bay. The government wants the foreign miners to sell controlling stake in ventures to local blacks, which is obviously frowned up on by all. The companies, given the uncertain situation, have refrained from investing further in expansion activities in Zimbabwe.

The country cannot access foreign credit as the ZIDERA Act passed by the United States in 2001 blocks US entities from trading with certain Zimbabwean institutions and individuals This has forced the US representatives in lending agencies like World Bank, IMF, IFC, and ADB to take a favorable stance when it comes to Zimbabwean credit requests.

That said, where there's a will there's a way. And since this story refuses to go away, it probably means that Zimbabwe will definitely give it the old college try. Once again, the question is not what happens in Zimbabwe, but elsewhere, should the experiment prove to be even remotely successful.

Hyperinflation

International Monetary Fund

Reserve Currency

World Bank

A week ago we presented the idea floated by once hyperinflationary Zimbabwe, oddly jeered by most, that the country is seeking to move to a gold-backed currency, adding, somewhat surrealistically, that the "days of the US dollar as the world's reserve currency are numbered." And if anyone should know a hyperinflationary basket case, it's Zimbabwe. Well, today this bizarre story just went fuller retard, after the country announced that it may exchange diamonds for gold "so that it can have a gold-backed currency, according to a recent proposal from the governor of Zimbabwe’s central bank." Indeed we speculated previously why: "Zimbabwe, a country rich in natural resources, took so long to figure out that it was nothing but a puppet in the hands of western monetary interests." Well, others are now getting this idea - Commodity Online reports that "The country is a resource hub: It sits on gold reserves worth trillions. It has the world’s second largest reserves of platinum, has got alluvial diamonds that can fetch the nation $2 billion annually and even boasts of chrome and coal deposits." And since Zimbabwe is now fully on board this whole "pioneering" thing perhaps it should just go ahead and create the first diamond-platinum backed currency. Just don't give China and Russia ideas about floating a new reserve currency that actually has real commodity backing. What's that, you say? They are launching one soon? Oh well.

From Commodity Online:

The Zimbabwean dollar is no longer in active use after it was officially suspended by the government due to hyperinflation. The United States dollar, South African rand, Botswanan pula, Pound sterling, and Euro are now used instead. The US dollar has been adopted as the official currency for all government transactions with the new power-sharing regime, says Wikipedia.

But the central bank of Zimbabwe—Reserve Bank of Zimbabwe (RBZ)—believes that the US dollar is no longer stable.

According to Dr Gideon Gono, RBZ Chief, the inflationary effects of United States’ deficit financing of its budget may impact foreign countries and would lead to a resistance of the green back as a base currency; cited newzimbabwe.com.

Writing in a blog in New Zimbabwe, Gilbert Muponda, an entrepreneur based out of Zimbabwe has welcomed the proposal of a gold-backed Zimbabwean currency. He has applauded the proposal of the central bank governor to sell diamonds for gold.

On the other hand, for the country to move to some semblance of a gold standard, it may wish to consider shifting form a despotic dictatorship controlled by Robert Mugabe to something a little less "centrally planned."

The government’s protectionist measures have kept the mining companies at bay. The government wants the foreign miners to sell controlling stake in ventures to local blacks, which is obviously frowned up on by all. The companies, given the uncertain situation, have refrained from investing further in expansion activities in Zimbabwe.

The country cannot access foreign credit as the ZIDERA Act passed by the United States in 2001 blocks US entities from trading with certain Zimbabwean institutions and individuals This has forced the US representatives in lending agencies like World Bank, IMF, IFC, and ADB to take a favorable stance when it comes to Zimbabwean credit requests.

That said, where there's a will there's a way. And since this story refuses to go away, it probably means that Zimbabwe will definitely give it the old college try. Once again, the question is not what happens in Zimbabwe, but elsewhere, should the experiment prove to be even remotely successful.

Thursday, May 19, 2011

FOREX: Japan Enters Recession, NZ Dollar Gains on Budget Surplus Outlook

Critical Levels

The Euro was little changed in overnight trade, rising to test above 1.43 to the US Dollar in the first part of the session as Asian stocks followed Wall Street higher to weigh on safety-linked demand for the greenback but promptly erasing the advance as shares reversed course in the aftermath of Japan’s GDP figures (see below). The British Pound mirrored the single currency, rising toward the 1.62 figure but failing to hold ground ahead of the opening bell in Europe. We are looking for EURUSD and GBPUSD selling opportunities and remain long USDJPY.

Asia Session: What Happened

UK Retail Sales headline the calendar in European hours, with expectations calling for core receipts (excluding auto fuel) to rise 2.2 percent in the year through April, marking the strongest outcome in three months. While encouraging, the release is unlikely to prove particularly supportive for the British Pound.

Echoing concerns raised in an analogous release from the BRC, an outsized year-on-year increase this time around seems to substantially owe to a particularly weak result in April 2010, where retail conditions were marred by uncertainty ahead of the UK general election and which didn’t include Easter holiday spending, as this year’s numbers will. An unexpected drop in the Nationwide Consumer Confidence gauge reported overnight will do little to stem skepticism.

Sizing up sentiment trends, stock index futures tracking key European bourses are well into positive territory ahead of the opening bell, but this likely follows the corrective bounce on Wall Street rather than a genuine reversal of recent weakness. Indeed, as noted in our weekly fundamental trends monitor, “markets don’t move in straight lines and some fits and starts [are] to be expected” as the emerging risk-averse trend centered on the unwinding of bets dependent on cheap QE2 funding ahead of the program’s June expiry runs into short-term bargain hunters.

Meanwhile, futures tracking the S&P 500 are essentially flat, pointing to indecision after the rebound heading into yesterday’s FOMC minutes release. With that outcome proving to be largely a non-event as expected, the larger risk-negative trend established over the past two weeks looks ready to resume, giving the US Dollar scope to resume its advance against the major currencies.

For real time news and analysis, please visit http://www.dailyfx.com/real_time_news

CCY | SUPPORT | RESISTANCE |

| EURUSD | 1.4084 | 1.4330 |

| GBPUSD | 1.6016 | 1.6274 |

The Euro was little changed in overnight trade, rising to test above 1.43 to the US Dollar in the first part of the session as Asian stocks followed Wall Street higher to weigh on safety-linked demand for the greenback but promptly erasing the advance as shares reversed course in the aftermath of Japan’s GDP figures (see below). The British Pound mirrored the single currency, rising toward the 1.62 figure but failing to hold ground ahead of the opening bell in Europe. We are looking for EURUSD and GBPUSD selling opportunities and remain long USDJPY.

Asia Session: What Happened

GMT | CCY | EVENT | ACT | EXP | PREV |

| 23:01 | GBP | Nationwide Consumer Confidence (APR) | 43 | 46 | 45 (R+) |

| 23:50 | JPY | Gross Domestic Product (QoQ) (1Q) | -0.9% | -0.5% | -0.8% (R-) |

| 23:50 | JPY | Gross Domestic Product Annualized (1Q) | -3.7% | -1.9% | -3.0% (R-) |

| 23:50 | JPY | Gross Domestic Product Deflator (YoY) (1Q) | -1.9% | -1.8% | -1.6% |

| 23:50 | JPY | Nominal Gross Domestic Product (QoQ) (1Q) | -1.3% | -0.7% | -1.1% (R-) |

| 23:50 | JPY | Housing Loans (YoY) (1Q) | 2.7% | - | 3.2% |

| 1:00 | AUD | Consumer Inflation Expectation (MAY) | 3.3% | - | 3.5% |

| 1:30 | AUD | Average Weekly Wages (QoQ) (FEB) | 1.0% | 1.2% | 1.4% (R+) |

| 1:30 | AUD | Average Weekly Wages (YoY) (FEB) | 3.8% | 3.8% | 3.9% |

| 2:00 | NZD | New Zealand Releases Annual Budget | - | - | - |

| 4:30 | JPY | Industrial Production (MoM) (MAR F) | -15.5% | - | -15.3% |

| 4:30 | JPY | Industrial Production (YoY) (MAR F) | -13.1% | - | -12.9% |

| 4:30 | JPY | Capacity Utilization (MoM) (MAR) | -21.5% | - | 2.9% |

| 5:30 | JPY | Nationwide Department Store Sales (YoY) (APR) | -1.5% | - | -14.7% |

| 5:30 | JPY | Tokyo Department Store Sales (YoY) (APR) | -5.5% | - | -21.5% |

Currency markets were relatively quiet in overnight trade, with the New Zealand Dollar outperforming after the Finance Minister Bill English said in the annual Budget that the government will return to surplus by June 2015, easing sovereign debt fears that have plagued the island nation, prompting ratings agencies Standard and Poor’s and Fitch to put to downgrade their credit outlooks to “negative” in November 2010 and July 2009, respectively. The currency rose as much as 0.9 percent against its top counterparts.

Japanese Gross Domestic Product figures showed the country entered into recession as the economy shrank 0.9 percent I the first quarter having slumped 0.8 percent in the three months through December 2010. The outcome had little immediate impact on the Japanese Yen despite the worse-than-expected outcome considering a generally dismal print was widely expected considering the island nation suffered its worst earthquake on record during the period in question. The disaster took a heavy toll on economic activity, shuttering businesses and disrupting export deliveries. Still, the currency would go on to underperform as bearish momentum built throughout the session.

Euro Session: What to Expect

GMT | CCY | EVENT | EXP | PREV | IMPACT |

| 8:30 | GBP | Retail Sales ex Auto Fuel (MoM) (APR) | 0.8% | 0.2% | Medium |

| 8:30 | GBP | Retail Sales ex Auto Fuel (YoY) (APR) | 2.2% | 0.9% | Medium |

| 8:30 | GBP | Retail Sales inc Auto Fuel (MoM) (APR) | 0.8% | 0.2% | Medium |

| 8:30 | GBP | Retail Sales inc Auto Fuel (YoY) (APR) | 2.5% | 1.3% | Medium |

| 9:00 | EUR | Italian Current Account (€) (MAR) | - | -6337M | Low |

| 9:00 | CHF | ZEW Survey (Expectations) (MAY) | - | 8.8 | Low |

| 10:00 | GBP | CBI Trends Selling Prices (MAY) | - | 36 | Low |

| 10:00 | GBP | CBI Trends Total Orders (MAY) | -9 | -11 | Low |

UK Retail Sales headline the calendar in European hours, with expectations calling for core receipts (excluding auto fuel) to rise 2.2 percent in the year through April, marking the strongest outcome in three months. While encouraging, the release is unlikely to prove particularly supportive for the British Pound.

Echoing concerns raised in an analogous release from the BRC, an outsized year-on-year increase this time around seems to substantially owe to a particularly weak result in April 2010, where retail conditions were marred by uncertainty ahead of the UK general election and which didn’t include Easter holiday spending, as this year’s numbers will. An unexpected drop in the Nationwide Consumer Confidence gauge reported overnight will do little to stem skepticism.

Sizing up sentiment trends, stock index futures tracking key European bourses are well into positive territory ahead of the opening bell, but this likely follows the corrective bounce on Wall Street rather than a genuine reversal of recent weakness. Indeed, as noted in our weekly fundamental trends monitor, “markets don’t move in straight lines and some fits and starts [are] to be expected” as the emerging risk-averse trend centered on the unwinding of bets dependent on cheap QE2 funding ahead of the program’s June expiry runs into short-term bargain hunters.

Meanwhile, futures tracking the S&P 500 are essentially flat, pointing to indecision after the rebound heading into yesterday’s FOMC minutes release. With that outcome proving to be largely a non-event as expected, the larger risk-negative trend established over the past two weeks looks ready to resume, giving the US Dollar scope to resume its advance against the major currencies.

For real time news and analysis, please visit http://www.dailyfx.com/real_time_news

Monday, May 16, 2011

Forex: Euro To Face Increased Volatility As EU Finance Ministers Convene, U.S. Dollar Price Action Remains Mixed

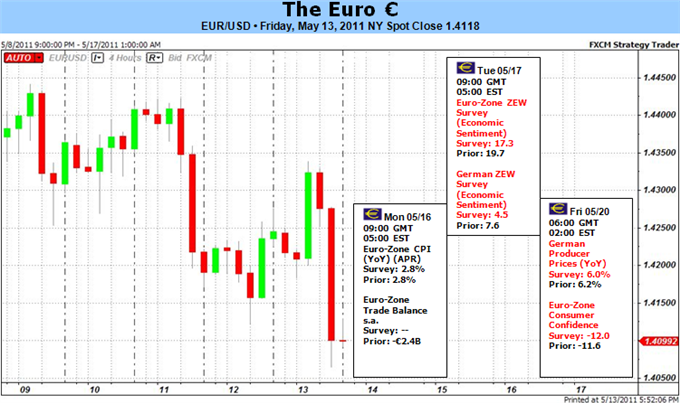

Currency traders showed a fairly muted reaction to the Euro-Zone consumer price report even as the core rate of inflation topped forecasts in April, and the bullish sentiment underlying the single-currency may continue to deteriorate over the near-term as the central bank softens its hawkish outlook for inflation. The EUR/USD pared the overnight advance to 1.4147 as European Central Bank board member Ewald Nowotny sees inflation falling back towards the 2% target in 2012, and gave back the early-morning rally to 1.4152 to maintain the narrow downward trending chancel carried over from earlier this month. As market participants speculate Greece to restructure its debt, the EU will certainly have to step up its efforts to address the sovereign debt crisis, and currency traders will certainly turn their focus to the two-day meeting in Brussels as euro-area finance ministers attempt to finalize the European Stability Mechanism.

However, the arrest of International Monetary Fund Managing Director Dominique Strauss-Kahn appears to have rattled market sentiment as the region continues to seek foreign aid, and the lack of urgency to contain the risk for contagion will continue to dampen demands for the single-currency as the European periphery face record-high financing costs. In turn, the Governing Council may have little choice but to delay its exit strategy further and the EUR/USD looks poised to test 1.4000 in the coming days as it searches for support. According to Credit Suisse overnight index swaps, market participants are still pricing a zero percent chance for a 25bp rate hike in June, but see borrowing costs in Europe increasing by nearly 100bp over the next 12-months as growth and inflation gather pace.

The British Pound bounced back from a low of 1.6161 coming into the North American trade, and the small rebound in the GBP/USD may gather pace over the next 24-hours of trading as the headline reading for inflation is expected to grow at a faster pace April. As the Bank of England sees consumer prices hitting an annualized 5.0% this year, the central bank is likely to draw up a hawkish tone in its policy meeting minutes which are due out on Wednesday, and currency traders will surely keep a close eye on the vote count as Governor Mervyn King changes his tune for future policy. If we see a growing shift within the MPC, a 5-4 split within the committee should spark a bullish reaction in the British Pound, but the majority may look to carry out their wait-and-see approach for most of 2011 given the ongoing weakness within the real economy. As a result, the GBP/USD may trend sideways throughout the beginning of the week, but comments from the central bank is likely to dictate future price action for the sterling as investors weigh the prospects for future policy.

The U.S. dollar continued to face mixed price action against its major counterparts, but the reserve currency may regain its footing during the North American trade as investors continue to scale back their appetite for risk. As market participants show a subdued reaction to the Empire manufacturing report, risk sentiment should dictate price action across the currency market, and the greenback should benefit from safe-haven slows as equity futures point to a lower open for the U.S. market.

However, the arrest of International Monetary Fund Managing Director Dominique Strauss-Kahn appears to have rattled market sentiment as the region continues to seek foreign aid, and the lack of urgency to contain the risk for contagion will continue to dampen demands for the single-currency as the European periphery face record-high financing costs. In turn, the Governing Council may have little choice but to delay its exit strategy further and the EUR/USD looks poised to test 1.4000 in the coming days as it searches for support. According to Credit Suisse overnight index swaps, market participants are still pricing a zero percent chance for a 25bp rate hike in June, but see borrowing costs in Europe increasing by nearly 100bp over the next 12-months as growth and inflation gather pace.

The British Pound bounced back from a low of 1.6161 coming into the North American trade, and the small rebound in the GBP/USD may gather pace over the next 24-hours of trading as the headline reading for inflation is expected to grow at a faster pace April. As the Bank of England sees consumer prices hitting an annualized 5.0% this year, the central bank is likely to draw up a hawkish tone in its policy meeting minutes which are due out on Wednesday, and currency traders will surely keep a close eye on the vote count as Governor Mervyn King changes his tune for future policy. If we see a growing shift within the MPC, a 5-4 split within the committee should spark a bullish reaction in the British Pound, but the majority may look to carry out their wait-and-see approach for most of 2011 given the ongoing weakness within the real economy. As a result, the GBP/USD may trend sideways throughout the beginning of the week, but comments from the central bank is likely to dictate future price action for the sterling as investors weigh the prospects for future policy.

The U.S. dollar continued to face mixed price action against its major counterparts, but the reserve currency may regain its footing during the North American trade as investors continue to scale back their appetite for risk. As market participants show a subdued reaction to the Empire manufacturing report, risk sentiment should dictate price action across the currency market, and the greenback should benefit from safe-haven slows as equity futures point to a lower open for the U.S. market.

Sunday, May 15, 2011

Euro on the Verge of Financial Panic but Risk Appetite Still Holding

If ever there were a good example of the equilibrium of risk / reward in the markets, it would be the euro. Even though the shared currency does not maintain the highest yield amongst its peers (the Australian and New Zealand dollars are still offering a better return); it nevertheless holds itself out to be as resilient as its more valuable counterparts. What makes this performance particularly remarkable though is that this inherent optimism is maintained despite the euro’s facing some of the worst fundamental risks of any of the majors markets. The financial troubles facing Greece and Portugal specifically present problems that run to the very core of euro and the European Monetary Union it represents. In the balance between the fear and greed that defines this (and every) market, there is clearly a dislocation – and it is primarily centered on the under-appreciation of present and growing risks. If we want to gauge when the euro will finally capitulate, our focus should be expectations for instability.

My general outlook for the euro has been a bearish one for some time; but that does not necessarily mean we should immediately trade that bias. There have been historically many periods when the investing masses have tolerated excessive risk or disregarded exceptional return to maintain a comfortable trend. This seems to defy fundamental reason; but more accurately, it reflects the markets’ prejudices – and the market defines price. As for the financial troubles facing the Euro-region, the problems are well-known which may lead many to believe that they are fully priced in. Yet, the full potential fallout from a debt/currency crisis is unknown and the ECB’s effort to keep inflation under wraps has given short-term speculators a convenient distraction. Should we see the meeting of Eurogroup Finance Ministers over the first two days of the week come up short on a solution for Greece, Portugal and Ireland; it could further bring the region’s troubles into relief.

To understand the market impact from the event; we need to know what is at stake. At the forefront of the discussion, we have Greece which forced the region to the next leg of the financial devolution. Though officials will not to admit as much, it is not unlikely that the country indeed threatened its EU counterparts that it would withdrawal from the monetary restraints (which come along with the currency) unless further accommodation was made. Few other scenarios would encourage such a prompt and compliant vow to offer the member further aid (regardless of the European Commission’s updated forecast for Greece to post a wide-target missing, 9.5 percent debt to GDP ratio this year). However, accommodation for this already deeply indebted nation would certainly encourage Ireland and Portugal (who have recently seen political upheaval as citizens vote on anti-austerity beliefs) to demand the same. With more than 250 billion euros in aid already extended, further rounds of accommodation will only push us closer to the breaking point.

Will this particular meeting provide the shock that changes the balance in the market? The probability is not high. As we have seen with previous meetings with similar stakes, policy officials are adept at playing to funding and currency markets that preoccupied with passive returns with flimsy promises. With Germany refusing further amendment without equivalent guarantees of progress, it is even more unlikely that we will see purposeful improvement. That said, a rebound for the euro is a more likely scenario; but it will die out quickly as few are expecting a roaring recovery from the region’s troubles. The deciding factor may actually lie outside of the euro’s own fundamental influence. Should we see global risk appetite falter, traders will abandon the most overvalued and troubled assets – the euro among them. - JK

Wednesday, May 11, 2011

Trade Deficit in U.S. Probably Widened in March as Energy Prices Increased

The U.S. trade deficit probably widened in March as rising commodity prices boosted the value of imports, economists said before a report today.

The gap grew by 2.6 percent to $47 billion, the biggest in nine months, from $45.8 billion in February, according to the median forecast of 72 economists surveyed by Bloomberg News.

Crude oil costs that surged above $100 a barrel for the first time in more than a year and a 9.4 percent drop in the dollar will probably keep driving up the cost of imports. At the same time, the weaker currency is making American goods more competitive to customers in emerging markets from Argentina to China, benefiting manufacturers like United Technologies Corp. (UTX) and Caterpillar Inc. (CAT)

“We should see ongoing strength in U.S. exports because of the weakness of the dollar,” said Sal Guatieri, a senior economist at BMO Capital Markets in Toronto. “Trade should have a fairly neutral impact on the U.S. economy” as both imports and exports climb.

The Commerce Department’s report is due at 8:30 a.m. in Washington. Estimates ranged from deficits of $43 billion to $49.3 billion. The gap has widened from a decade-low of $24.9 billion reached in May 2009 during the recession.

A barrel of crude oil on the New York Mercantile Exchange averaged $102.98 in March, up from $89.74 in February. It reached an intraday high of $114.83 on May 2 and has since dropped on concern world growth may slow.

Dollar’s Influence

The dollar’s 9.4 percent drop from June 7, 2010, to March 31 against a weighted basket of currencies from the country’s biggest trading partners is making American-made goods cheaper abroad and foreign-made goods more expensive in the U.S.

Combined with growth in emerging economies such as Brazil and India, the decrease in the dollar will probably continue to help lift exports.

United Technologies, maker of Carrier air conditioners, last month said 2011 sales would be at the high end of its forecast as pent-up demand stokes growth globally.

“As we look across the globe, we see end markets are improving,” Chief Financial Officer Gregory Hayes said on an April 20 conference call. “Emerging markets continue to lead worldwide economic growth and UTC’s businesses are capitalizing on this opportunity.”

Manufacturing companies have outperformed the broader market this year. The Standard & Poor’s 500 Industrials Index has gained 11 percent this year, compared with a 7.9 percent increase for the S&P 500 Index.

Global Growth

Caterpillar said it expects global economic growth this year of about 4 percent, with developing countries expanding by 6.5 percent and the U.S. by 3.5 percent. The company plans about $3 billion in capital spending this year, with more than half of that in the U.S.

Caterpillar posted first-quarter profit that topped analysts’ estimates and raised its full-year earnings forecast as sales surged in developing countries. The Peoria, Illinois- based maker of earthmoving equipment said its outlook would have been higher had it not been for the March 11 earthquake in Japan.

“Our facilities in Japan were not damaged by the earthquake and tsunami, but many of our suppliers in Japan were,” Chief Executive Officer Doug Oberhelman said on a conference call April 29. “As a result, we are experiencing sporadic production disruptions at many of our facilities around the world.”

A growing trade deficit with China is prompting U.S. officials to seek a solution. Top-ranking delegates from the two countries met in Washington this week amid U.S. pressure for China to allow the yuan to rise against the dollar.

U.S. Treasury Secretary Timothy F. Geithner and Chinese Vice Premier Wang Qishan pledged May 9 to tackle currency, financial services and trade conflicts between the world’s two biggest economies at the start of the two-day Strategic and Economic Dialogue.

Bloomberg Survey

===========================================

Trade Federal

Balance Budget

$ Blns $ Blns

===========================================

Date of Release 05/11 05/11

Observation Period March March

-------------------------------------------

Median -47.0 -41.0

Average -47.0 -50.2

High Forecast -43.0 -35.0

Low Forecast -49.3 -80.0

Number of Participants 72 25

Previous -45.8 -82.7

-------------------------------------------

4CAST Ltd. -47.1 -41.0

ABN Amro -48.3 ---

Action Economics -47.0 -41.0

Aletti Gestielle -47.2 ---

Ameriprise Financial -47.5 ---

Banesto -45.8 ---

Barclays Capital -47.5 -41.0

Bayerische Landesbank -48.0 ---

BBVA -45.3 -45.0

BMO Capital Markets -48.8 -62.5

BNP Paribas -48.5 ---

BofA Merrill Lynch -48.0 -80.0

Briefing.com -45.0 -41.0

Capital Economics -48.5 ---

CIBC World Markets -46.5 ---

Citi -47.0 -40.0

Commerzbank AG -48.5 ---

Credit Agricole CIB -46.8 ---

Credit Suisse -47.0 ---

Daiwa Securities America -48.0 -40.0

DekaBank -47.0 ---

Desjardins Group -48.8 -70.0

Deutsche Bank Securities -44.0 ---

Deutsche Postbank AG -46.0 ---

DZ Bank -47.0 ---

Fact & Opinion Economics -46.0 -62.0

First Trust Advisors -44.3 ---

FTN Financial -46.0 ---

Goldman, Sachs & Co. -48.0 -41.0

Helaba -43.0 ---

High Frequency Economics -43.0 -65.0

Hugh Johnson Advisors -47.0 ---

Ibersecurities -46.0 ---

IDEAglobal -47.5 -60.0

IHS Global Insight -48.0 ---

Informa Global Markets -46.2 -41.0

Insight Economics -47.5 ---

Intesa-SanPaulo -47.0 ---

J.P. Morgan Chase -46.4 -41.0

Janney Montgomery Scott -47.8 ---

Jefferies & Co. -47.5 ---

Landesbank Berlin -46.0 ---

Landesbank BW -45.0 ---

Maria Fiorini Ramirez -47.5 ---

MF Global -47.5 -41.0

Mizuho Securities -48.0 ---

Moody’s Analytics -48.3 ---

Morgan Keegan & Co. -46.6 ---

Morgan Stanley & Co. -45.0 ---

National Bank Financial -48.0 ---

Natixis -46.4 ---

Nomura Securities -43.0 -42.0

Nord/LB -46.2 ---

Parthenon Group -46.9 ---

Pierpont Securities -46.4 -42.0

PNC Bank -48.0 ---

Raiffeisenbank International -46.0 ---

Raymond James -48.5 -41.0

RBC Capital Markets -47.7 ---

RBS Securities -46.5 ---

Scotia Capital -48.0 ---

Societe Generale -47.7 ---

Standard Chartered -47.0 ---

State Street Global Markets -47.4 -70.0

Stone & McCarthy Research -48.9 -35.0

TD Securities -46.0 -62.0

UBS -49.0 -41.0

University of Maryland -48.8 -70.0

Wells Fargo & Co. -49.3 ---

WestLB AG -46.8 ---

Westpac Banking Co. -48.0 ---

Wrightson ICAP -47.0 ---

===========================================

To contact the reporter on this story: Bob Willis in Washington at bwillis@bloomberg.net

The gap grew by 2.6 percent to $47 billion, the biggest in nine months, from $45.8 billion in February, according to the median forecast of 72 economists surveyed by Bloomberg News.

Crude oil costs that surged above $100 a barrel for the first time in more than a year and a 9.4 percent drop in the dollar will probably keep driving up the cost of imports. At the same time, the weaker currency is making American goods more competitive to customers in emerging markets from Argentina to China, benefiting manufacturers like United Technologies Corp. (UTX) and Caterpillar Inc. (CAT)

“We should see ongoing strength in U.S. exports because of the weakness of the dollar,” said Sal Guatieri, a senior economist at BMO Capital Markets in Toronto. “Trade should have a fairly neutral impact on the U.S. economy” as both imports and exports climb.

The Commerce Department’s report is due at 8:30 a.m. in Washington. Estimates ranged from deficits of $43 billion to $49.3 billion. The gap has widened from a decade-low of $24.9 billion reached in May 2009 during the recession.

A barrel of crude oil on the New York Mercantile Exchange averaged $102.98 in March, up from $89.74 in February. It reached an intraday high of $114.83 on May 2 and has since dropped on concern world growth may slow.

Dollar’s Influence

The dollar’s 9.4 percent drop from June 7, 2010, to March 31 against a weighted basket of currencies from the country’s biggest trading partners is making American-made goods cheaper abroad and foreign-made goods more expensive in the U.S.

Combined with growth in emerging economies such as Brazil and India, the decrease in the dollar will probably continue to help lift exports.

United Technologies, maker of Carrier air conditioners, last month said 2011 sales would be at the high end of its forecast as pent-up demand stokes growth globally.

“As we look across the globe, we see end markets are improving,” Chief Financial Officer Gregory Hayes said on an April 20 conference call. “Emerging markets continue to lead worldwide economic growth and UTC’s businesses are capitalizing on this opportunity.”

Manufacturing companies have outperformed the broader market this year. The Standard & Poor’s 500 Industrials Index has gained 11 percent this year, compared with a 7.9 percent increase for the S&P 500 Index.

Global Growth

Caterpillar said it expects global economic growth this year of about 4 percent, with developing countries expanding by 6.5 percent and the U.S. by 3.5 percent. The company plans about $3 billion in capital spending this year, with more than half of that in the U.S.

Caterpillar posted first-quarter profit that topped analysts’ estimates and raised its full-year earnings forecast as sales surged in developing countries. The Peoria, Illinois- based maker of earthmoving equipment said its outlook would have been higher had it not been for the March 11 earthquake in Japan.

“Our facilities in Japan were not damaged by the earthquake and tsunami, but many of our suppliers in Japan were,” Chief Executive Officer Doug Oberhelman said on a conference call April 29. “As a result, we are experiencing sporadic production disruptions at many of our facilities around the world.”

A growing trade deficit with China is prompting U.S. officials to seek a solution. Top-ranking delegates from the two countries met in Washington this week amid U.S. pressure for China to allow the yuan to rise against the dollar.

U.S. Treasury Secretary Timothy F. Geithner and Chinese Vice Premier Wang Qishan pledged May 9 to tackle currency, financial services and trade conflicts between the world’s two biggest economies at the start of the two-day Strategic and Economic Dialogue.

Bloomberg Survey

===========================================

Trade Federal

Balance Budget

$ Blns $ Blns

===========================================

Date of Release 05/11 05/11

Observation Period March March

-------------------------------------------

Median -47.0 -41.0

Average -47.0 -50.2

High Forecast -43.0 -35.0

Low Forecast -49.3 -80.0

Number of Participants 72 25

Previous -45.8 -82.7

-------------------------------------------

4CAST Ltd. -47.1 -41.0

ABN Amro -48.3 ---

Action Economics -47.0 -41.0

Aletti Gestielle -47.2 ---

Ameriprise Financial -47.5 ---

Banesto -45.8 ---

Barclays Capital -47.5 -41.0

Bayerische Landesbank -48.0 ---

BBVA -45.3 -45.0

BMO Capital Markets -48.8 -62.5

BNP Paribas -48.5 ---

BofA Merrill Lynch -48.0 -80.0

Briefing.com -45.0 -41.0

Capital Economics -48.5 ---

CIBC World Markets -46.5 ---

Citi -47.0 -40.0

Commerzbank AG -48.5 ---

Credit Agricole CIB -46.8 ---

Credit Suisse -47.0 ---

Daiwa Securities America -48.0 -40.0

DekaBank -47.0 ---

Desjardins Group -48.8 -70.0

Deutsche Bank Securities -44.0 ---

Deutsche Postbank AG -46.0 ---

DZ Bank -47.0 ---

Fact & Opinion Economics -46.0 -62.0

First Trust Advisors -44.3 ---

FTN Financial -46.0 ---

Goldman, Sachs & Co. -48.0 -41.0

Helaba -43.0 ---

High Frequency Economics -43.0 -65.0

Hugh Johnson Advisors -47.0 ---

Ibersecurities -46.0 ---

IDEAglobal -47.5 -60.0

IHS Global Insight -48.0 ---

Informa Global Markets -46.2 -41.0

Insight Economics -47.5 ---

Intesa-SanPaulo -47.0 ---

J.P. Morgan Chase -46.4 -41.0

Janney Montgomery Scott -47.8 ---

Jefferies & Co. -47.5 ---

Landesbank Berlin -46.0 ---

Landesbank BW -45.0 ---

Maria Fiorini Ramirez -47.5 ---

MF Global -47.5 -41.0

Mizuho Securities -48.0 ---

Moody’s Analytics -48.3 ---

Morgan Keegan & Co. -46.6 ---

Morgan Stanley & Co. -45.0 ---

National Bank Financial -48.0 ---

Natixis -46.4 ---

Nomura Securities -43.0 -42.0

Nord/LB -46.2 ---

Parthenon Group -46.9 ---

Pierpont Securities -46.4 -42.0

PNC Bank -48.0 ---

Raiffeisenbank International -46.0 ---

Raymond James -48.5 -41.0

RBC Capital Markets -47.7 ---

RBS Securities -46.5 ---

Scotia Capital -48.0 ---

Societe Generale -47.7 ---

Standard Chartered -47.0 ---

State Street Global Markets -47.4 -70.0

Stone & McCarthy Research -48.9 -35.0

TD Securities -46.0 -62.0

UBS -49.0 -41.0

University of Maryland -48.8 -70.0

Wells Fargo & Co. -49.3 ---

WestLB AG -46.8 ---

Westpac Banking Co. -48.0 ---

Wrightson ICAP -47.0 ---

===========================================

To contact the reporter on this story: Bob Willis in Washington at bwillis@bloomberg.net

Subscribe to:

Posts (Atom)